Banks have been bad losers, through and through. Ask those in the blockchain and crypto space. First, they rivaled, and failed, next they blocked. And when nothing worked, they arm-twisted governments into introducing regulations to stifle their growth. Last we heard, they’re now trying to up their game and “incorporate” and “integrate”

Here’s how the financial bigshots played their games at suppressing the rise of cryptocurrency.

Verbal Attacks on Crypto

Back in 2014, government agencies worked to devise ways to control Bitcoin. The biggest banks of Wall Street were frustrated over regulations, as that would grant them a legal entity – this, in turn, could pose a threat to their industry. Therefore, they resorted to sowing the seed of apprehension and doubt.

During the World Economic Forum in Davos the same year, Jamie Dimon, the chief executive of JPMorgan Chase, the nation’s largest bank, expressly dismissed Bitcoin as a “terrible” store of value that was an instrument of illicit activities. At a discussion table on violations of Iran sanctions, H. Rodgin Cohen, the pre-eminent finance lawyer, warned the state’s regulators with the hint that the federal government was “very worried” about Bitcoin and its utilization.

Needless to say, the efforts in public dismissal, criticism, and discouragement tanked. In 2015, New York’s Department of Financial Services started issuing licenses for Bitcoin businesses. There exist over 75 million users of Bitcoin. This is up several notches from around three million recorded seven years ago. Also, the number of digital assets has boomed.

Also Read: HashCash Offers Blockchain-Biometric Solution for Banking and Finance Corporations

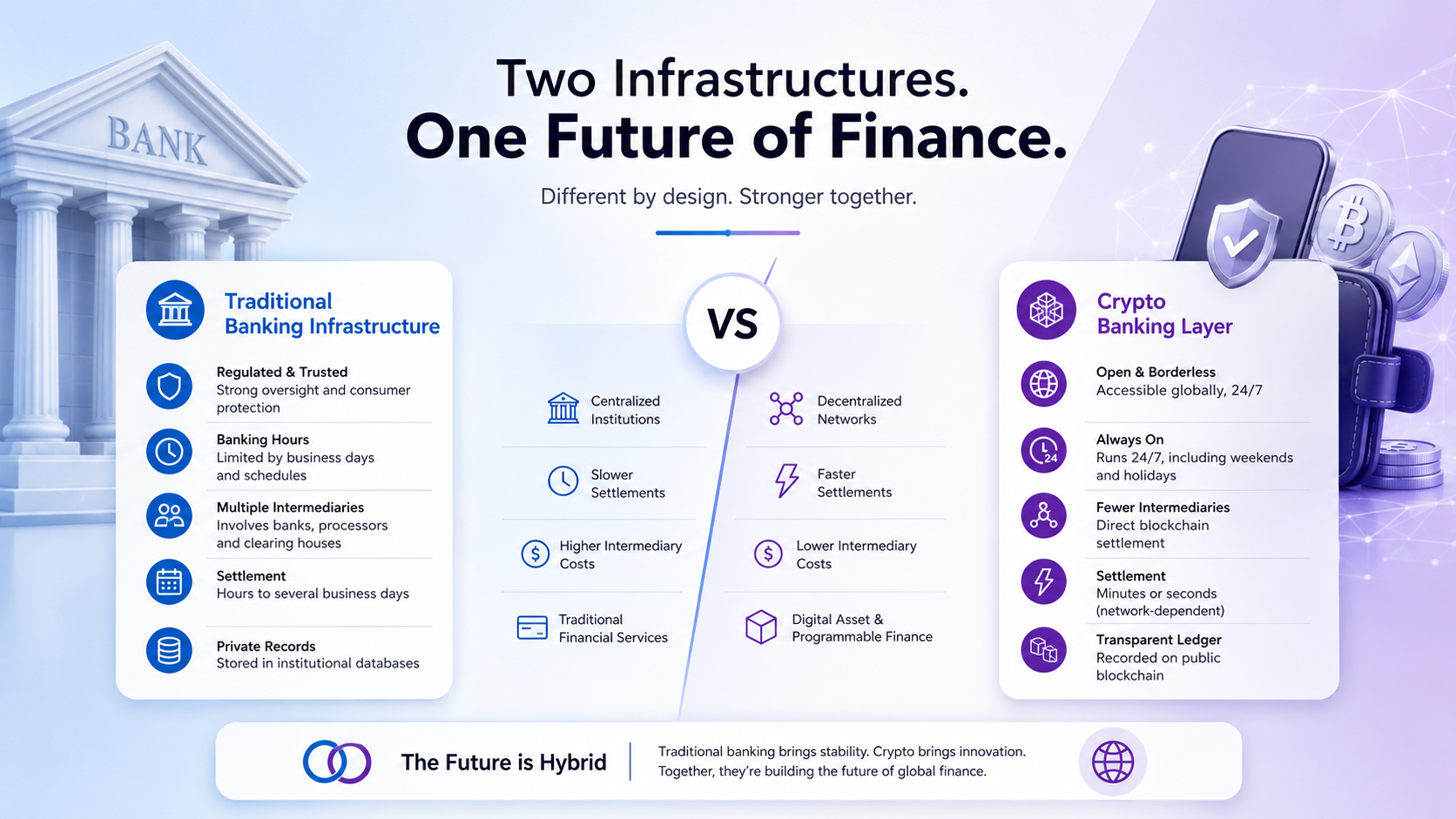

Then versus Now

Of late it’s in the news that the banks are racing each other in the drive to align themselves to accommodate digital assets as a financial investment instrument, as a payment method, and as a representation of a business concept. Banks want to lap up the monetary gains from this industry. Their approach is bi-directional. Firstly they seek to experiment with cryptocurrency offerings, scooping sufficiently large gains. On the other hand, they must lobby regulators to enact regulations that side with the banks.

Many banks now offer cryptocurrency investment opportunities to their wealthy clients. Others weigh trading desks for Bitcoin. JPMorgan has flagged off its own digital currency in 2019.

Also Read: Central Bank of Brazil Considers Digital Real To Keep Up With The Digitization of Global Economy

And then

Instead of advising regulators against harsh impositions on cryptocurrencies, the banking industry heads now whine. According to them, regulators have not acted promptly enough, and their inaction costs banks heavily in their mission to compete.

However, in reality, it was their initial skepticism that cost them time. A parallel financial world is popping up around the traditional banking industry. Cryptocurrency start-ups are set to launch credit cards and loans. People and businesses around the world have rapidly warmed up to digital currencies. So much so that even some governments have found hope. El Salvador recently adopted Bitcoin as legal tender.

After so much, the Federal Reserve, is considering the launch its own digital currency to curb the growth trajectory of cryptocurrencies.

Finally

The traditional banking system has exercised the power and control over people’s money historically. Banks have for centuries indirectly wielded the governance over people and their wealth. The control over the flow of money in their local economies happened by taking deposits, then lending some of that money to other customers.

The rise of secondary markets for loans ensure that banks could lend even more against the deposits they had by selling the loans to investors after they were made and freeing space on their balance sheets to do more lending. At every step of the way, they made money.

This centralized control of wealth would start to leak once the cryptocurrencies assumed their full-fledged run, this is what scares the governments and more so, the banks. They can already foresee their waning relevance in the financial markets today and pressing their powers to put a stop to it.

No Comment