Digital money is no longer just an idea for the future. It is already changing how people send payments, shop online, and move money across borders. Among the many forms of digital currency, two terms often create confusion: STABLECOINS and CENTRAL BANK DIGITAL CURRENCIES (CBDCS).

Although both exist in digital form and often derive their value from a national currency, different organizations develop, manage, and use them for distinct purposes.

If you’ve ever wondered whether they’re the same thing, this guide will help you understand the differences in simple terms.

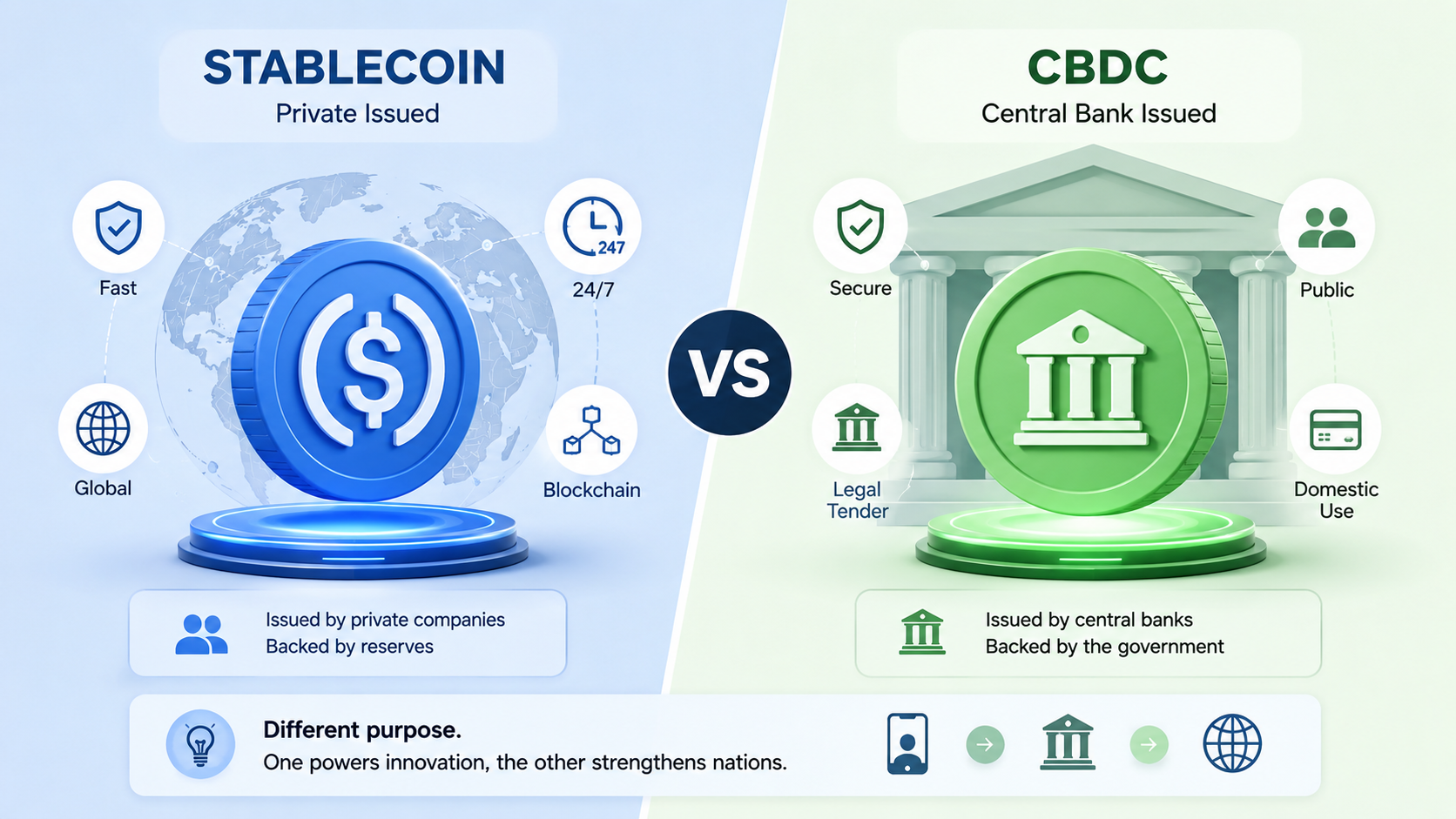

What Is Stablecoin?

A stablecoin is a digital asset designed to maintain a stable value, usually by being tied to a traditional currency like the dollar, euro, or another fiat currency. The main goal is to reduce the price swings that are common in many digital assets.

Imagine you want to send money to a friend living in another country. Instead of waiting several days for a bank transfer, you could send a stablecoin within minutes. Since its value stays relatively stable, your friend receives almost the same purchasing power you intended to send.

Most stablecoins are issued by private organizations and operate on blockchain networks, allowing transactions to be recorded transparently and securely.

What Is a CBDC?

A Central Bank Digital Currency, or CBDC, is a digital version of a country’s official currency issued directly by its central bank. Unlike stablecoins, CBDCs are government-backed and represent legal tender.

Think of it as the digital form of the cash already in your wallet. Instead of printing paper notes, the central bank creates digital currency that people can use for everyday payments.

Many countries are currently researching or testing CBDCs to improve payment systems, reduce transaction costs, and support financial inclusion. According to the Bank for International Settlements, more than 90% of central banks have explored CBDCs in some form, showing how seriously governments are taking this technology.

Stablecoin vs CBDC: The Main Differences

Although both aim to make digital payments easier, their foundations are very different.

|

Feature |

Stablecoin |

CBDC |

|

Issuer |

Private organization |

Central bank |

|

Backing |

Usually reserves or other assets |

National government |

|

Legal Tender |

Usually No |

Yes |

|

Blockchain |

Often public or private blockchain |

Depends on the country’s design |

|

Primary Goal |

Fast digital transactions and innovation |

Modernize national payment systems |

The biggest difference comes down to who issues and controls the currency. Stablecoins rely on private issuers, while CBDCs are managed by governments through their central banks.

A Simple Example

Imagine two people each receive 100 digital units.

The first person receives 100 units of a stablecoin issued by a private organization. Its value is designed to stay close to the national currency, but users rely on the issuer to maintain that stability.

The second person receives 100 units of a CBDC issued directly by the country’s central bank. Those digital units are officially part of the national currency itself.

Both people can make digital payments, but the source of trust is completely different. One depends on a private issuer, while the other depends on the government.

Advantages of Stablecoins

Stablecoins have become popular because they offer several practical benefits.

- They allow fast transfers across borders.

- They can operate around the clock without traditional banking hours.

- They reduce the impact of price volatility compared to many other digital assets.

- Developers can integrate them into blockchain-based applications and digital financial services.

These features make stablecoins attractive for international payments, online commerce, and decentralized financial systems.

Advantages of CBDCs

CBDCs are designed with national financial systems in mind rather than private innovation.

Some of their potential advantages include:

- Faster domestic payment systems.

- Lower transaction costs for consumers and businesses.

- Better access to digital payments for people without traditional banking services.

- Improved efficiency in distributing government payments or benefits.

Because CBDCs are backed by central banks, they may also strengthen public confidence in digital forms of money.

Which One Is Better?

There isn’t a single winner because they solve different problems.

Stablecoins often focus on flexibility, global accessibility, and innovation. They are commonly used in blockchain ecosystems where speed and interoperability are important.

CBDCs, on the other hand, focus on strengthening national payment infrastructure. Governments may use them to improve existing financial systems while maintaining monetary control.

Rather than replacing one another, they could eventually coexist. A person might use a CBDC for everyday domestic purchases while using stablecoins for international transactions or blockchain-based services.

Challenges Both Face

Despite their benefits, neither technology is without challenges.

Stablecoins depend heavily on trust in the issuer and the quality of the assets backing them. Questions about transparency and regulation continue to shape public discussions.

CBDCs face different concerns. Many people wonder how governments will protect privacy and balance oversight with individual financial freedom.

In addition, both technologies must handle cybersecurity risks, regulatory compliance, and large-scale adoption before they can reach their full potential.

If you’re interested in learning more about how digital currencies fit into the future of payments, the International Monetary Fund provides useful research and educational resources.

Final Thoughts

Stablecoins and CBDCs may look similar because both exist digitally and often represent the value of traditional money. However, different principles govern their design.

Private organizations typically create stablecoins to enable efficient digital transactions, while central banks issue CBDCs as official digital versions of national currencies.

As digital finance continues to evolve, understanding this distinction will become increasingly important. Whether you’re an investor, business owner, or simply curious about the future of money, understanding the differences between these two forms of digital currency will help you better understand the financial systems shaping today’s economy.

No Comment